HIT Consultant – Read More

What You Should Know:

– If 2024 was a year of correction, 2025 was the year of crystallization. The tremors of innovation have settled into bedrock infrastructure, and the market has responded with a distinct roar.

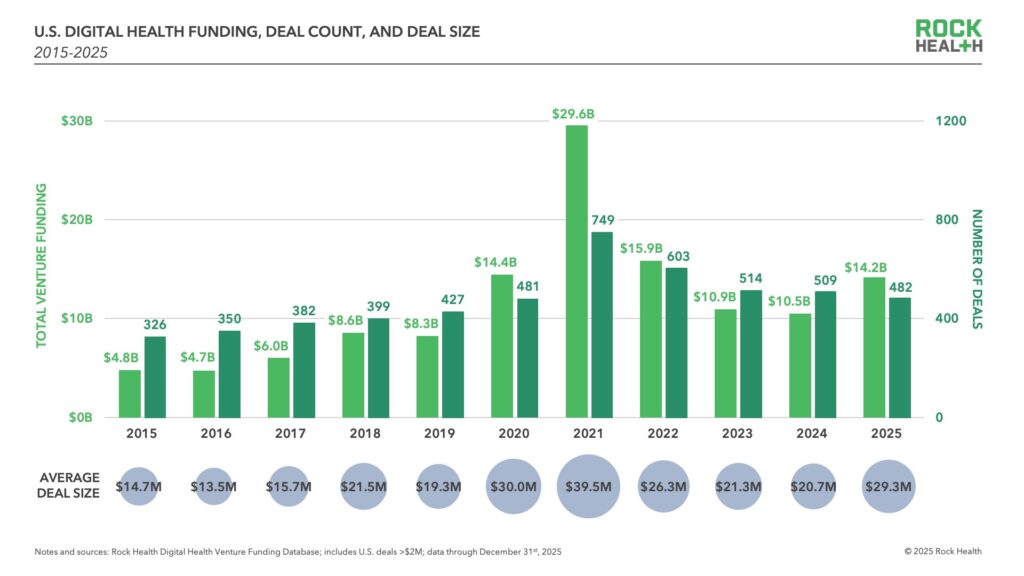

– Annual funding for U.S. digital health startups climbed to $14.2Bin 2025, a meaningful 35% increase over the previous year, according to Rock Health’s annual year-end report. While we haven’t returned to the fever dream of pandemic-era peaks, the data reveals a “new normal” that is roughly 36% above the pre-pandemic baseline of 2019.

– But the headline growth masks a starker reality: a market deeply divided between the “haves” and the “have-nots.”

2025 Market Overview: Capital Concentration and Mega Deals

The headline $14.2B figure masks a tightening at the top: capital is flowing to fewer companies in larger quantities. While funding rose by $3.7B, the total deal count actually dropped by 5% (482 vs. 509 in 2024).

- The Rise of Mega Deals: Raises over $100M accounted for 42% of all funding, the highest proportion since 2021.

- Average Deal Size: Jumped to $29.3M, up from $20.7M in 2024, reflecting the outsized influence of a few top-tier players.

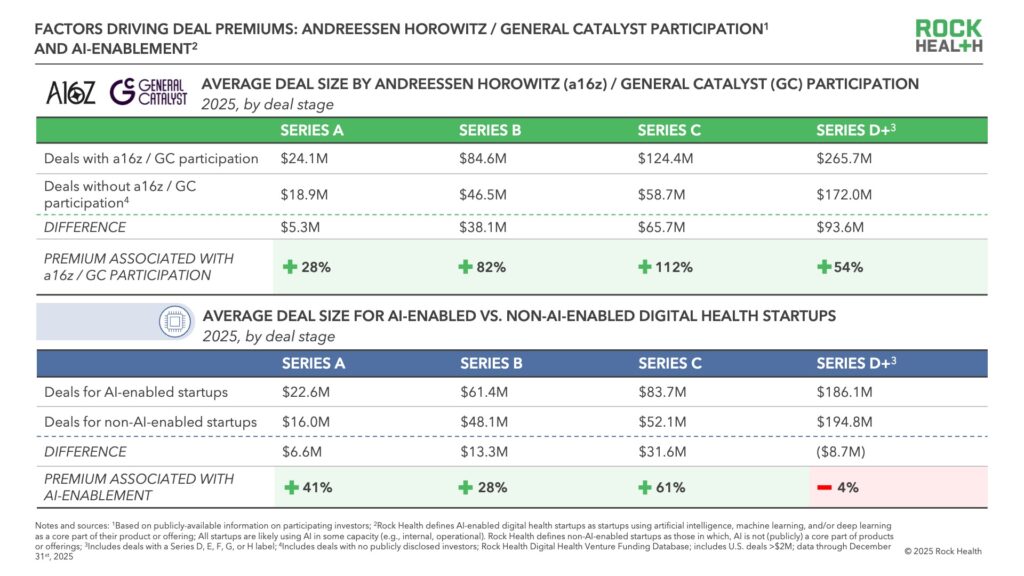

- The “Mega Fund” Premium: Deals involving firms like a16z or General Catalyst commanded significant premiums, with Series A rounds averaging $24.1M vs. $18.9M for those without their participation.

The AI and Wellness Premiums

AI-enabled companies captured 54% of total funding in 2025, commanding a 19% premium on average deal size. This was most pronounced at Series C, where AI startups saw a 61% premium. Simultaneously, wellness and fitness startups (led by Oura’s $900M round) vaulted to the third-most funded value proposition as D2C lab testing and longevity became mainstream consumer priorities.

The Spectrum of Exits: M&A Surges and IPOs Return

M&A activity hit 195 deals, a 61% increase over 2024, driven by both growth-stage “shopping sprees” and distressed exits for companies operating in the “murky middle”.

- IPO Breakthrough: Five companies—Hinge Health, Omada Health, Heartflow, Carlsmed, and Profusa—broke the three-year public exit drought in 2025.

- PE Momentum: Private equity healthtech spend saw a reported 600% increase as firms placed major bets on established “winners”.

2026 Outlook: Policy as the New Wildcard

As we look toward 2026, the Trump administration’s policy agenda will likely act as the next major market shaper.

- CMMI ACCESS Model (July 2026): A potential game-changer offering consistent payments for chronic condition management, allowing startups to bypass some traditional reimbursement hurdles.

- Deregulation: The recent removal of Biden-era AI transparency requirements signals a faster, albeit potentially riskier, path to market for AI tools.

For founders, the message from 2025 is clear: The tide is rising, but only for those who can prove they are building infrastructure, not just features. In 2026, you are either a platform, or you are a feature on someone else’s roadmap.